Employer FAQs on the Rise of GLP-1 Drugs for Weight Loss and the Workplace Impact

The rise of prescription medications used for weight loss has reshaped conversations about employer-sponsored health benefits and raised many new questions for employers. You have likely heard of Ozempic and other GLP-1 drugs and their ability to promote significant weight loss, but you may still be unsure of how to design your health plan in a way that balances cost factors and compliance issues with employee attraction and retention goals. Read on for answers to your top questions related to this current hot topic.

General Background

What are GLP-1 drugs?

Glucagon-like peptide-1 (GLP-1) receptor agonists are a class of prescription medications that mimic the effects of the natural GLP-1 hormone and help control blood sugar levels, slow digestion, and regulate appetite. GLP-1 drugs have been used for decades to treat Type 2 diabetes. In recent years, they have been expanded for other uses, including weight loss and weight management, which has caused their popularity to explode.

Semaglutides, such as Ozempic and Wegovy, are one type of GLP-1 drug. Tirzepatides, such as Mounjaro and Zepbound, are technically classified differently because they incorporate agonists of both GLP-1 and another hormone called glucose-dependent insulinotropic polypeptide (GIP). For simplicity, this Insight uses the term “GLP-1 drugs” to refer to both semaglutides and tirzepatides.

Most GLP-1 drugs are injectable medications, though a growing number of semaglutides are becoming available in pill form.

Has the FDA approved GLP-1 drugs used for weight loss and weight management?

The US Food & Drug Administration has approved only some GLP-1 drugs for weight loss and long-term weight management and only when certain conditions are met. For example, the FDA has approved the following drugs when combined with diet and exercise:

- Wegovy and Zepbound (trade names) to reduce excess body weight and maintain weight reduction long term in adults with obesity or adults who are overweight and have at least one weight-related condition;

- Wegovy to “reduce the risk of cardiovascular death, heart attack and stroke in adults with cardiovascular disease and either obesity or overweight” (FDA news release); and

- Zepbound to treat moderate to severe obstructive sleep apnea in adults with obesity (FDA news release).

As of publication, Ozempic and Mounjaro are not approved by the FDA for weight loss or weight management (though clinicians sometimes prescribe these drugs for such off-label uses).

How common is GLP-1 drug use among adults in the US?

In a recent survey, 18% of adults said they had used GLP-1 drugs for weight loss or to treat diabetes or other chronic conditions, while 12% said they were currently using them.

Employer Impact

Are employer-sponsored health plans required to cover GLP-1s for weight loss?

Generally speaking, no. Employers generally have discretion in deciding which benefits to cover under their health plans. However, employers that sponsor fully insured plans must choose from plan options that comply with state insurance mandates. See the next Q/A below for more on state insurance requirements related to GLP-1 drugs.

In addition, while most group health plans (whether fully insured or self-funded) are subject to many federal laws, including the preventive-care mandates under the Affordable Care Act (learn more here), none require employers to cover GLP-1 drugs for either diabetes treatment or weight loss.

Do any state insurance laws mandate coverage of GLP-1 drugs for weight loss?

In the context of private, fully insured health insurance plans, North Dakota is currently the only state that requires coverage of GLP-1 drugs weight-related treatment under certain conditions. Specifically:

- North Dakota updated its essential health benefit (EHB) benchmark plan under the Affordable Care Act to require, beginning in 2025, prescription drug coverage of GLP-1s and GIPs as therapy for prevention of diabetes and treatment of insulin resistance, metabolic syndrome or morbid obesity.

- However, this change applies only to all individual and small group ACA-covered insurance plans in North Dakota; it does not apply to grandfathered plans or large group plans.

While other states have considered measures related to GLP-1 drug coverage, these proposals have dropped off since last year, and most pertain to state Medicaid programs or coverage for state employees. However, New Hampshire lawmakers recently introduced a bill (SB455-FN) that would, if passed, require certain fully insured commercial health plans to cover GLP-1 medications under certain circumstances. California and Maine considered similar legislation last year, but those bills failed to pass.

How common is it for employer-sponsored plans to cover GLP-1 drug for weight loss?

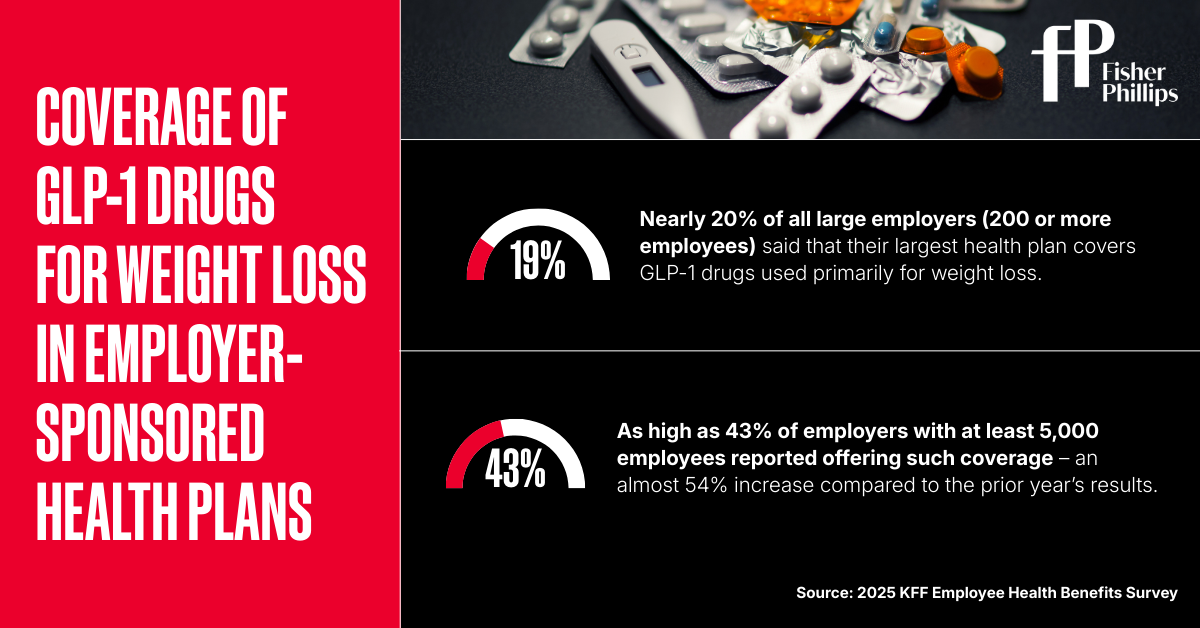

According to the 2025 KFF Employee Health Benefits Survey:

- Nearly 20% of all large employers (200 or more employees) said that their largest health plan covers GLP-1 drugs used primarily for weight loss. This represents little change from survey results in 2024.

- As high as 43% of employers with at least 5,000 employees reported offering such coverage – an almost 54% increase compared to the prior year’s results.

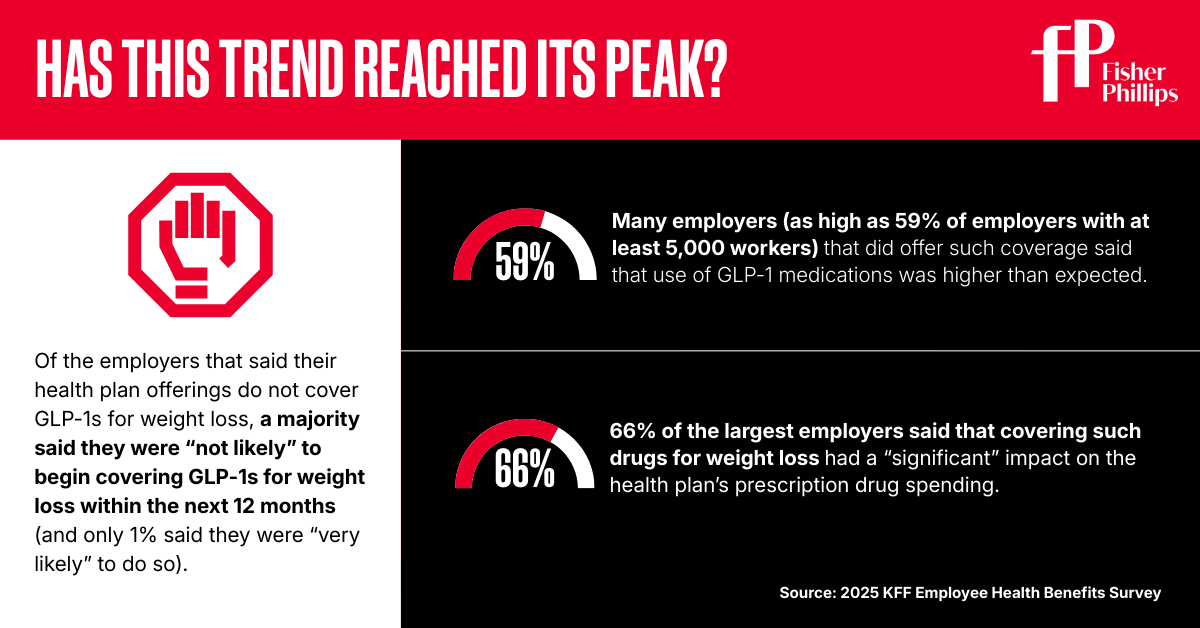

However, the KFF report indicates that this new trend might have reached its peak. Of the employers that said their health plan offerings do not cover GLP-1s for weight loss, a majority said they were “not likely” to begin covering GLP-1s for weight loss within the next 12 months (and only 1% said they were “very likely” to do so).

Further, many employers (as high as 59% of employers with at least 5,000 workers) that offered such coverage said that use of GLP-1 medications was higher than expected, and 66% of the largest employers said that covering such drugs for weight loss had a “significant” impact on their health plan’s prescription drug spending.

“Discussions with individual employers suggest that some have stopped covering these medications for weight loss, with a few even tightening up coverage for those with diabetes,” according to the report. “While concerns over the negative health impacts of obesity remain, they are now in competition with concerns about the high cost and proper use of GLP‑1agonist medications, particularly at a time when other cost pressures may be growing.”

When such coverage is offered, is it common to impose conditions to qualify for it?

Many employers that offer health plans that cover GLP-1 drugs impose conditions that plan participants must meet to qualify for such coverage. This could include meeting clinical eligibility criteria, trying lower-cost or alternative interventions before coverage is approved, or requiring prior authorization.

For example, in the KFF survey discussed above, 34% of the employers that reported offering such coverage said that plan participants must “meet with a dietician, case manager, or therapist, or participate in a lifestyle program” in order to receive the coverage.

May an employer-sponsored health plan offer indication-based coverage for GLP-1 medications?

It’s complicated – this is an evolving area of the law. Employers should keep in mind that indication-based coverage decisions (such as covering GLP-1 drugs for diabetes treatment but not for treatment of obesity or other conditions, such as addiction) can potentially raise concerns under the Americans with Disabilities Act (ADA), the ACA, HIPAA’s nondiscrimination requirements, or the Mental Health Parity and Addiction Equity Act, among other laws.

- Currently, no federal law explicitly bars weight-based discrimination, and most federal appeals courts have held that obesity (unless caused by an underlying health condition) is not a protected disability under the ADA.

- However, district courts have produced mixed decisions on that issue, and the EEOC has filed disability-related lawsuits in the past on behalf of morbidly obese employees. In addition, some state and local antidiscrimination laws include weight as a protected class.

- Several employees have sued health insurance companies for excluding coverage of GLP-1 medications prescribed solely to treat obesity, arguing that such obesity exclusion constitutes disability discrimination under the ACA. However, these lawsuits have so far targeted insurers or third parties, not employers directly, and have mostly been unsuccessful.

In sum, employers should take extra caution when considering GLP-1 coverage for some conditions, but not others. Work with your FP counsel to ensure compliance with these laws.

Are there alternative ways to support employees who seek weight loss medications?

Employers that are unwilling or unable to offer health plan coverage of GLP-1 drugs for weight management may consider offering consumer-driven health plans and tax-advantaged accounts, such as health savings accounts (HSAs) or flexible spending accounts (FSAs).

If certain IRS conditions are met, HSAs and/or FSAs allow employees to use pre-tax dollars to pay for eligible prescription medications, and employers may opt to make contributions to such accounts, which employees can apply toward such costs. Employers that go this route should educate employees and communicate very clearly about the eligibility conditions and documentation required by the plan and under IRS rules.

Conclusion

Employers must consider many factors, including costs, compliance, and employee expectations, when determining whether to offer GLP-1 coverage under the health plans they sponsor. You should work with your FP counsel when making these decisions, as this is a developing area that can potentially trigger various compliance issues, including issues beyond the scope of these FAQs.

If you have questions, please contact your Fisher Phillips attorney, the authors of this Insight, any attorney in our Employee Benefits and Tax Practice Group. Make sure you are subscribed to Fisher Phillips’ Insight System to get the most up-to-date information on this and other employment topics directly to your inbox.

Related People